BEYOND COVID-19...Fostering Resilience In the Chemical Supply Chain.

Traces of chemicals can be found in almost every product we touch or use. Chemicals are very fundamental in the production of essential products such as medicine, detergents, sanitizers, and protective equipment. On an economic level, the chemical industry’s contribution towards development and growth has been predominate over the years.

How agile is your chemical supply chain, now and beyond COVID-19?

In 2018, the GCC chemical industry recorded $84.1 billion in revenue with production capacity reaching 174.8 million tons, a contribution increase of 2.8% to the regional GDP. The International Council of Chemical Associations (ICCA) likewise revealed that the chemical industry, its payroll-induced and supply chain contributes $5 trillion to the global GDP creating over 120 million jobs globally.

The chemical industry has lately been hit hard on all sides mainly due to disruptions in the global supply chain caused by ongoing trade wars, global protectionism and, most recently, the COVID-19 pandemic. The latter has led to a decrease in demand for chemicals by up to 30% in the automotive, transportation and consumer products sectors - which is the hardest hit end-markets. COVID-19 has not only accentuated disruptions in global supply chains but also revealed the frailty of supply chains’ dependencies on Tier 1 and Tier 2 suppliers. Presently, the global supply chain system is categorized into three levels (Tiers 1, 2 and 3) and operates a liner model. This linear supply chain model presents little or no collaboration among the tiers. In addition, there is no visibility on the goods’ movement from one point of the chain to another at any given time. The COVID-19 pandemic (corona virus) which has uncovered many businesses’ vulnerabilities is now giving supply chain players and professionals a pause for thought. Could the ongoing disruption in the supply chain be the start of a new dawn to resilience? Let us discuss some of the current challenges.

1. Dependency and Concentration on Limited Supplier Network

Supply chain is about integration and dependency between different levels/players. Hence, any major dent in the process flow could lead to disruption. This has been the case in the wake of COVID-19. While news, reports cannot firmly explain how the corona virus began, the consensus so far points to Wuhan, China. The global supply chain industry has strongly relied on China. For many years, China, South Korea, and Italy have served as manufacturing hubs for over 12,000 industrial plants and warehouses belonging to the world’s leading 1,000 companies and their suppliers, according to a study by Resilinc. At the peak of the virus, most manufacturing plants in China were locked down to curtail the spread of the virus. Resilinc reports that close to 1,800 manufactured components trace their origin to Hubei - one of the first quarantined provinces in China. As revealed in a recent report by the GPCA, “China is one of the key destinations for GCC polyethylene exports and slowing demand would mean 6% lower imports from the GCC than in 2019 and 10% lower than forecasted for 2020 before the virus outbreak.” The pandemic’s impact on the industry became evident. Globally, the chemical supply chain market recorded a sharp decline in outputs leading to shortages of most raw materials and finished products. The petrochemical industry recorded a decline in output by 3.3% in March and 1.3 percent in April 2020. Similarly, Chemical Week’s CW75 index in April recorded a decrease by 23% quarter-to-quarter.

Indeed, this outbreak is a dreadful timing for chemical companies. The Industrial Average and FTSE 100 for Dow Jones, one of the largest multinational chemical manufactures, plunged to 3% or more than 1,000 points at the peak of the virus in China. Subsequently, the company’s earnings for Q1-2020 declined by 18% ($1.3 billion), according to recent reports. At its peak, the pandemic severely limited progress on the construction of BASF’s “Smart Verbund”, a new manufacturing complex in Zhanjiang, China. This clearly shows the crisis’ heavy impact on most companies. Although, positively, construction of the “Smart Verbund” project has resumed.

2. Lack of Visibility in the End-to-End Supply Chain

Global scenario planning based on data informed decisions and technology is yet another critical component of assessing supply chain options and preparing for the future. Unfortunately, most industries such as the chemical and supply chain are lurking behind when it comes to technology/digitisation. A recent GPCA Industry Insight stated that “the chemicals industry has been somewhat slow to use digital technologies effectively. Only 17% of chemical companies worldwide fit BCG’s definition of “digital champions”, in comparison to 23% of all companies in all industries”.

Furthermore, a recent survey by GEODIS based on the responses of 623 professionals in 17 countries revealed that 94% of supply chain managers disclosed the lack of full-fledged visibility on their supply chain processes. Moreover, GPCA reports that in 2018, the GGC chemical industry alone employed around 157,000 people. Notably, many of these jobs especially in the areas of manufacturing are more physical and demanded working on-site. However, with the implementation of preventive measures such as social distancing and reduced operational hours in the wake of COVID-19, production output further declined.

So, how can we ensure resilience in the supply chain? The next paragraphs will address these challenges mainly focusing on two factors - localisation and technology.

Even as the lockdown was lifted and China has reopened, a massive domestic demand shock is being realized in the wake of virus fear. “What is really important was that before March, everybody was expecting China to have a V-shaped recovery because it was actually (about) China’s supply disruption (initially), but now we are seeing this demand shock”, Bo Zhuang, Chief China Economist at TS Lombard, told CNBC news. As COVID-19 continues to impede industries, for the next normal, much sedulous effort is being considered for resilience which includes localisation.

1. Building a non-concentrated supply chain system (Localisation).

The interruption in China’s supply chain led to the shortage of medical supplies in most parts of the world including the United States (US). The shortage included personal protective equipment (PPEs) and most of the pharma drugs essential for treating persons infected with the coronavirus. Notably, China and India are the largest producers of active pharmaceutical ingredients (APIs) in the world. These APIs (chemical based) are mostly used in the production of generic/pharma drugs for human usage. A recent TIME.com report further states that over 90% of thermometer used in the USA are manufactured in China. However, at the peak of the virus leading to closure of manufacturing plants and border restrictions, most of these medical supplies were restricted in their place of origin, mostly Asian countries such as India and China, resulting in major disruptions in the supply chain and jeopardizing the delivery of these essential products. Authorities in India, for instant, placed restrictions on exports of 26 pharmaceuticals in bid of keeping stocks at the local front to fight the pandemic. “These are everyday products and the idea with the restrictions is to prevent a shortage in the country. But this will have a global impact”, stated Jatish Sheth - Director, Srushti Pharmaceuticals.

Moreover, most producers of medical supplies operate a just in time system as part of cost reduction, meaning that production is matched with the market demand to avoid excess inventory (buffer stocks). However, the risk this model brings is that any kind of disruption in the flow of products, as now caused by COVID-19, can lead to massive shortage of supplies. That is why many companies and industries are now forced to readjust their global supply chain model to a localisation effect.

So, why localisation?

A significant number of B2B purchasers/suppliers (72%) who participated in a recent survey conducted by Thomasnet.com responded that they would rather "always or generally" source materials locally, while 10.8% would rather "always or generally" source globally. Interestingly, the survey further revealed that almost half of the respondents (46.7%) have "rarely or never" sourced from global suppliers. This is not surprising as the preceding paragraph revealed the high frailty in depending on global suppliers due to problems with order fulfilment and timely deliveries. To address this while enhancing resilience in the supply chain, it has now become imperative to localize or operate production plants and source manufacturing elements closer to the end users’ markets. This way, we avoid unforeseen shortages in supplies and disruptions.

An article by GPCA disclosed the GCC chemical industry’s struggle in ensuring seamless flow “of chemical raw materials to reach production plants across the world where finished products are made”, being caused by growing global protectionism, trade tariffs and border closures. To curtail this, manufacturers and suppliers are now forced to rethink and readjust their global supply chain model to cushion such impacts in the future. How will they do this? It is about building agile supply chain processes by means of adding value to local productions to be more flexible and resilient. In the world of chemicals (pharmaceuticals), this could mean making room for buffer stocks, blending/mixing, packaging and repacking of chemical substances like APIs close to end users/distribution markets to further alleviate any shortfalls, for instant, in medical supplies which is partly caused by just-in-time production.

Furthermore, with localization, countries and companies tend to benefit from shorter supply chain procedures leading to swift movement of both raw and finished products and their seamless accessibility. Notably, in January 2018, the Abu Dhabi National Oil Company (ADNOC) introduced In-Country Value (ICV), a localisation program focusing on diversifying and supporting the region’s economic growth by means of safeguarding sourcing of products and services within the region. Another significant objective of the program is to further mitigate major supply chain risks in case of global supply chain disruptions by localizing crucial components of the supply/value chain which is prevalent today. Recently, companies like Abu Dhabi Ports, Abu Dhabi Department of Economic Development have also adopted the ICV system in their operations.

Another reason for localisation is associated with supply chain costs. Globally, the logistics industry operates at a high cost. A recent Frost & Sullivan study on “Urban Logistics Opportunities—Last-Mile Innovation”, projected global logistics expenditure reaching $10.6 trillion in 2020, disclosing that transportation will account for 70% of the cost.

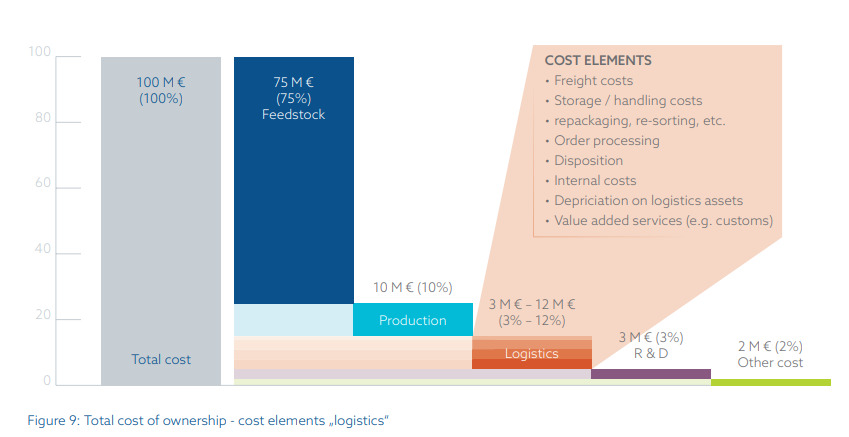

The below image from a study conducted by Kompetenzgruppe Chemielogistik (Leveraging Supply Chain for strategic advantage in the Chemical Industry) highlights the logistics costs for the largest chemical suppliers. As shown in the figures, logistics expenditure takes up to 3 - 12% of the total revenue and in severe instances up to 20%, according to the study.

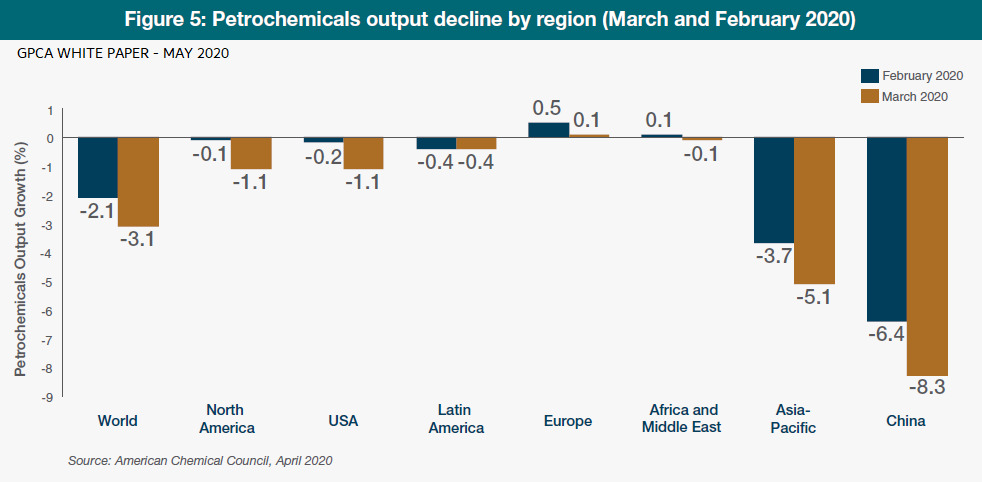

Ocean rates has likewise tripled more than the market average prior to the pandemic as revealed in a GPCA Whitepaper on May 2020. For instance shipping rates between India's port JNPT and Mundra to the Western Mediterranean and Northern Europe has increased by 25%. This is further raising concerns within the chemical supply chain.

To address this challenge, most companies, manufacturers, suppliers and even governments are putting mechanisms for regionalization/localisation as means to limit by possibly shifting their production plants and sourcing within their local domain, as well as investing in regional infrastructures. This will further result in a decrease of expenditure associated with purchasing and tariffs imposed on imports and exports.

For example, governments across the GCC region such as Saudi Arabia and the UAE have designated $ 1.1 trillion and $ 350 billion respectively towards infrastructural development between 2019 and 2038 aiming at improving local products as well as promoting local suppliers.

With localisation we do not only get to safeguard the supply chain process, but we also go the extra mile in protecting the environment. “In 2018, a total of 24% of global CO2 emissions from fuel combustion came from transportation”. Which means less cargo movements (products) mostly by ocean and air freight across regions will lead to reduction of the global carbon footprint caused by emissions during transportation.

2. Leveraging on supply chain visibility and robotics (digital supply chain)

To further accelerate resilience, especially in addressing the second challenge, would also mean that companies, manufacturers and players within supply and value chains need to adopt to the usage of the right technologies. Unfortunately, it was not until recently that industries such as the chemical industry began leveraging the benefits of technology in their operations. Today, technology-led business models are the game-changers leading the league as digitisation sweeps throughout most industries. “The time for organisations to act and implement digital is now,” states McKinsey. Notably top chemical companies leading this digital transformation includes BASF, SABIC, DOW, ARKEMA, SOLVAY.

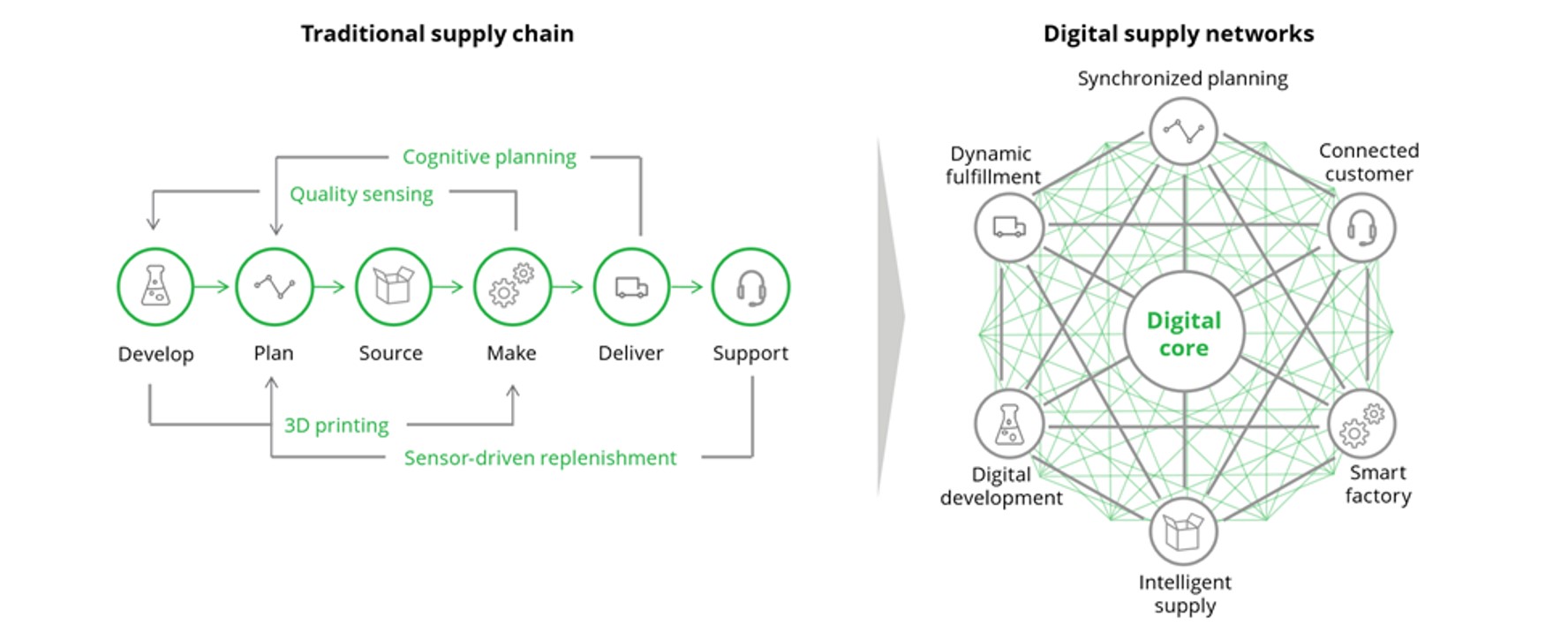

Presently, advanced supply chain technologies have buffered some of the economic headwinds that have hit the logistics field so far by improving end-to-end visibility, efficiency, and cost of operations across the supply chain. One digital element leading the wave on visibility across the industry is digital supply networks (DSN).

DSNs are integrated digital platforms/networks which accumulate and analyze data as well as events from the physical world and other digital platforms using advanced analytics, sensors, artificial intelligence allowing end-to-end agility, optimization, flexibility, visibility, and collaboration along the supply chain network. With continuous flow of information, DSNs enables companies to connect to their total supply network across the globe with complete access to readily available data/information such as customer demand, product quality and production capacity. According to experts of supply chain visibility at Quantzig “The ultimate goal of improving supply chain visibility is to progress and strengthen the supply chain by making information readily available to all stakeholders”.

Switching to DSNs from a traditional or linear supply chain model which lacks the dynanism of readily available information/data and integration, further means alleviating risks and errors such as wrong inventory counts, shipment delays or speed to market and overall lack of visibility and control. “Obtaining real-time visibility across all tiers in the supply chain can significantly increase speed to market, reduce capital expenditures and manage risk”, disclosed Jeff Dobbs, Global Sector Chair, Industrial Manufacturing – KPMG.

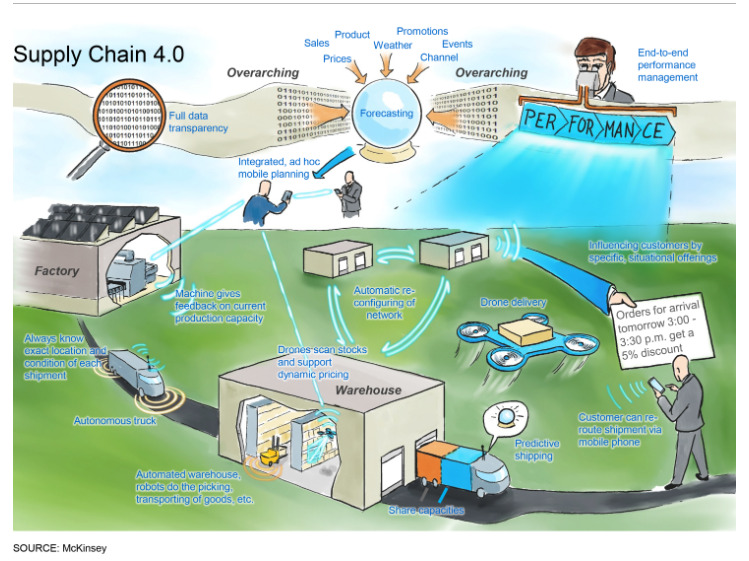

Another tech-innovation sweeping across the industry is Industry 4.0 – “a fourth industrial revolution enabled by digital and physical technologies”. It is characterized by the usage of advanced technologies such as the Internet of Things (IoT), robotics, 5G, and artificial intelligence (AI) by supply chain executives within the petrochemical and chemical industries to meet future logistics demands.

Companies who have adopted this smart innovation such as DOW, SABIC and BASF are witnessing major transformation across their value chain. For instance, BASF has introduced "BASF 4.0", a model that leverages on big data across its value chain to optimize cost and accelerate production and supply.

One of the previously mentioned challenges was regarding low outputs due to factories lockdowns and, consequently, leading to the stoppage of physical work. To address this issue, companies are now considering substituting parts of their human workforce with artificial intelligence (AI) software (robotics) which will become major enablers of automation with large economic impact, according to Mckinsey. The adoption of robotics will enable industry players to reduce dependency on the physical workforce from the manufacturing stage and fulfilment of orders in warehouses and use the human workforce for more strategic and developmental tasks. Thus, this will further mitigate any unforeseen shortages in the labor market. Other benefits include efficiency in production, the ability to control market demand either by scaling up or scaling down according to trends. The automotive industry is one of the early adopters of robotics.

Few examples of AI are Autonomous Mobile Robots (AMR), Automated guided vehicles (AGVs), Warehouse Management System (WMS), Drones and, Additive Manufacturing popularly referred to as 3D printing.

Moving forward…

Supply chain companies are now focusing on setting up crisis-management mechanisms. Given the variables discussed earlier implies that evolving from the impact COVID-19 has had will bring forward new winners and losers. Consequently, addressing the challenges taking into consideration localisation to reduce the dependencies on suppliers across the globe; and adoption of technologies to enable end-to-end visibility, process flexibility, and collaboration between suppliers, will reshape the future of global chemical supply chain networks and, subsequently, enhance their resilience.

How has your company been responding to recent supply chain disruptions? Let us have a discussion in the comments below.